Cash-to-Cash Cycle Time - Definition & Meaning

What is Cash-to-Cash Cycle Time?

The duration (measured in days) between the acquisition of a firm's inventory and the collection of accounts receivable for the sale of that inventory is called Cash-to-Cash Cycle time. Generally a company acquires an inventory on credit, which consequences in accounts payable. The company will then vend the inventory on credit, which leads to accounts receivable. Cash is thus not drawn in until the company pays the accounts payable and in turn, collects the accounts receivable. Therefore the cash conversion cycle calculates the time between outlay of cash and the recovery of the cash.

Calculation formula:

Cash to Cash Cycle Time = Days Sales Outstanding (DSO) + Inventory Days of Supply (IDS) - FIN - Days Payable Outstanding (DPO)

Example:

The inventory held by a business averages being on hand for 50 days, and its customers usually pay within 60 days. Offsetting the figures is an average payables period of say, 40 days. This results in the following cash to cash duration:

50 Days of inventory + 60 Days sales outstanding - 40 Days payables outstanding

= 70 Cash to cash days

This outcome states that a business must support its expenditures for a period of 70 days.

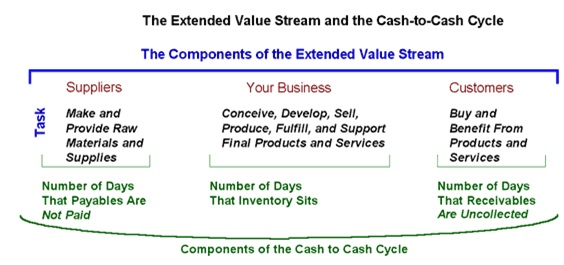

The below mentioned depicts the components of cash-to-cash cycle and its ability to represent how efficiently the extended value stream is operating

Image vitalentusa

Preferred outcome of Cash-to-Cash Cycle

In a strictly Lean system, there is no waste in any value stream. Goods are not manufactured or shipped to the buyer unless “pulled” and they are created by production systems that flow constantly without dependence on inventory. Raw materials are not acquired and processed unless a customer demands a completed output. Customers are billed and paid without delay upon receipt of a purchased product or service. In its ideal state, it is a just-in-time structure from the origins of its supply chain through to the receipt and payment by its customer. In this situation, the lean producer also pays its suppliers upon receipt as its clients pay upon delivery. There are zero receivables, inventory, and payables and thus zero day cash-to-cash cycle time. Although a zero-day cash-to-cash cycle is truly Lean, your business approaches its best attainable state gradually by reducing the cycle times it originally displays.

Hence, this concludes the definition of Cash-to-Cash Cycle Time along with its overview.

This article has been researched & authored by the Business Concepts Team. It has been reviewed & published by the MBA Skool Team. The content on MBA Skool has been created for educational & academic purpose only.

Browse the definition and meaning of more similar terms. The Management Dictionary covers over 1800 business concepts from 5 categories.

Continue Reading: