Materials Management - Definition & Importance

What is Materials Management?

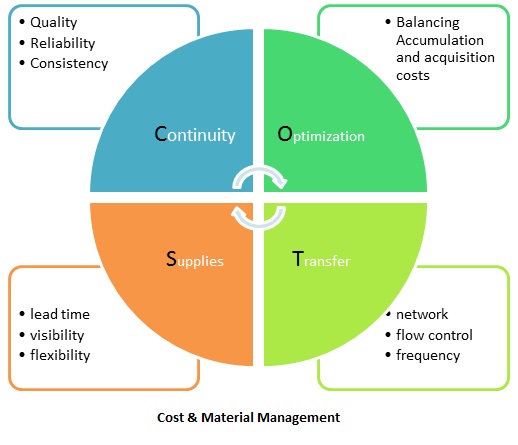

Materials management is a process adopted by companies to strategize, systematically arrange and monitor activities related with the flow of materials. Procurement of raw materials, its quantity, quality, supporting smaller products etc all fall under materials management. This is a critical function in ensuring streamlined operations & supply chain management.

Importance of Materials Management

Material, in the raw state, forms the chief share of the ending product and total cost of manufacturing. This is the most significant component of the completed product and hence, should be handled with supreme concern. Material cost influence to a huge degree the rate of production and also the quantity of proceeds which an entrepreneur eventually earns. Materials management is responsible with the purpose of policy making with consideration to procurement of the materials such as quality, amount, worth etc. and payout of the same to the individual jobs as and when it is necessary without any holdup.

Materials Management are also expressed by 5Rs:

- of the right quality

- in the right quantity

- at the right time

- from the right source

- at the right price

In many businesses, material cost represents about 70% of the whole cost of a manufactured goods. An efficient system of internal control should be introduced to keep material costs inside restrictions. This is probable only if an appropriate structure of material management is created.

Read More

Objectives of Materials Management

Materials management adds to the continued existence and earnings of an enterprise by providing sufficient supply of materials at the lowest achievable overheads. Some of the elemental objectives are discussed as below:

(i) Material choice: Right requirement of material and apparatus is dogged. In addition the material requirements in accord with sales programmer are reviewed. This can be done by examining the demand order of the buying section.

(ii) Low in service costs: It should attempt to keep the operating costs low and augment the profits without making any dispensation in quality.

(iii) Getting and scheming material safety and keeping it in good condition.

(iv) Issue the material receipt upon the acceptance by the appropriate authority.

(v) Recognition of spare stocks and taking suitable actions to create it.

The results of all these objectives are:

(i) Usual continuous supply of raw-materials to make sure the stability of production.

(ii)Providing cutback in purchasing and reducing waste leads to advanced output.

(iii)Minimized storage and stock control expenses.

(iv)Minimized cost of production in order to augment earnings.

(v) To buy items of finest quality at the most viable cost.

Hence, this concludes the definition of Materials Management along with its overview.

This article has been researched & authored by the Business Concepts Team. It has been reviewed & published by the MBA Skool Team. The content on MBA Skool has been created for educational & academic purpose only.

Browse the definition and meaning of more similar terms. The Management Dictionary covers over 1800 business concepts from 5 categories.

Continue Reading: